First-Time Homebuyer Loans

Buying your first home is a significant financial milestone. We provide the professional guidance and loan options necessary to help you work through the process with clarity and confidence, from your initial pre-approval to the day you receive your keys.

With a Bank of Utah Home Loan, You Can:

Start with Strategy

We explain each phase of the process clearly, so you’re prepared for every milestone from first conversation to closing.

Professional Advocacy

Our loan officers prioritize your long-term financial health, offering personalized advice to help you make informed decisions.

Tailored Loan Options

We review your budget and goals to match you with the loan program — such as FHA, VA, USDA or conventional — that fits best.

FHA = Federal Housing Administration • VA = Veterans Affairs • USDA = Department of Agriculture

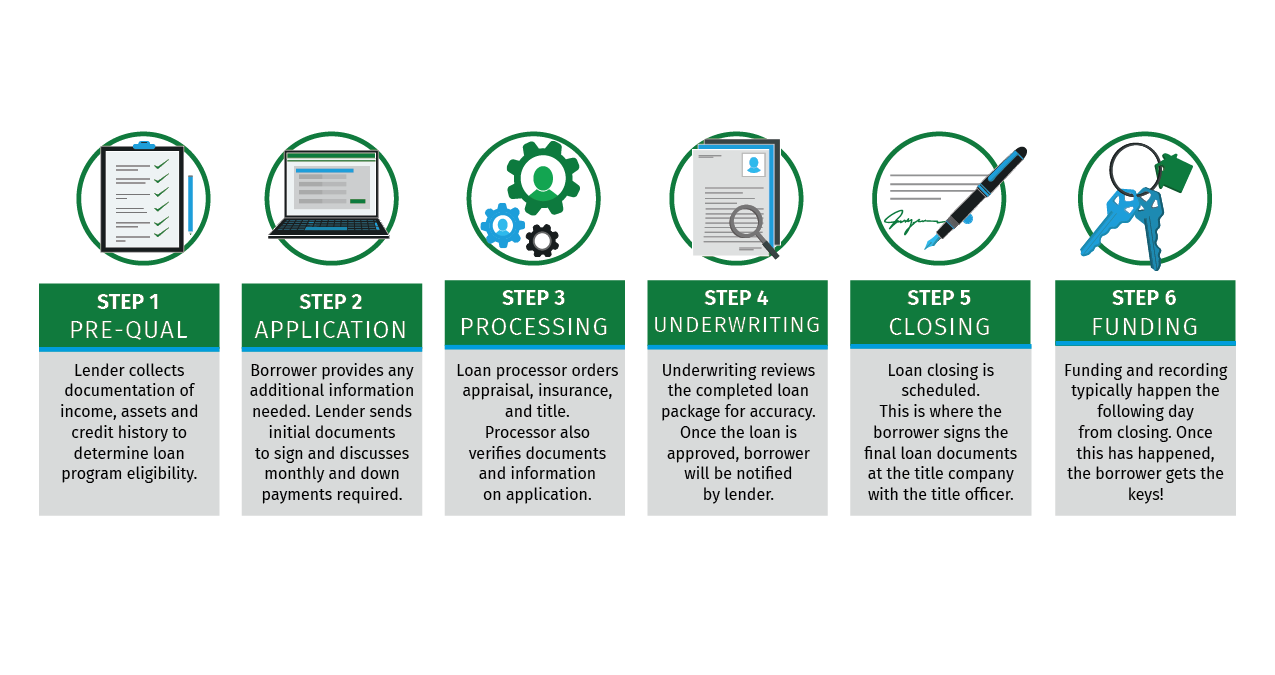

The Mortgage Process at a Glance

Understanding the sequence of a home loan helps you feel prepared for each stage.

Which Loan Program Is Right for You?

Every homebuyer’s financial picture is unique. Here’s how we commonly match buyers with the right loan program.

Starting with smaller savings?

A Federal Housing Administration (FHA) loan offers flexible credit requirements and down payments as low as 3.5 percent, making it a strong starting option for first-time buyers.

Have established credit?

A conventional loan offers long-term flexibility. It’s a strong fit if you have solid credit and want the option to cancel private mortgage insurance once you reach 20 percent equity.

Served in the military?

A Veterans Affairs (VA) loan recognizes your service with meaningful benefits, including potential options like zero down and no monthly mortgage insurance.

Buying in a qualifying area?

A U.S. Department of Agriculture (USDA) loan can be a strong zero-down option in designated rural or developing areas. Many Utah communities qualify based on location and income.

Explore Homebuyer Assistance Options

Utah Housing Corporation and other partners offer homebuyer assistance programs that can help with upfront costs such as down payment or closing expenses. In some cases, assistance may be available for up to $20,000, depending on the program and eligibility.

Connect With a Loan OfficerPrograms are administered by Utah Housing Corporation and other agencies. Income, purchase price and other limits apply.

Frequently Asked Questions

Talk With Us About Your Next Step

Have questions or want to walk through your options? Connect with a loan officer or start your application online when it works for you.

All loans subject to credit and underwriting approval, additional terms and conditions apply. Specific eligibility requirements exist for down payment assistance, FHA, VA, and USDA programs.